The year 2017 has been yet another landmark year for the Indian energy sector. At a national aggregate level India … More

Girish Shivakumar

The year 2017 has been yet another landmark year for the Indian energy sector. At a national aggregate level India … More

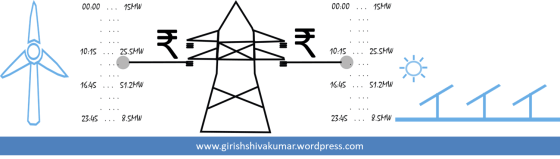

“Wind and solar power projects are powered by natural sources and hence their tariffs should be low”, is a general … More

According to various report sources India has a population of about 200-300 million without access to electricity i.e. about 15-20% … More

Ministry of Power (MoP) recently invited comments on a consultation paper on issues related to Open Access (OA). Electricity Act … More

Energy Efficiency Services Limited (EESL) could come across as yet another government initiative that is unrelenting in its pursuit of … More

Economic Policy of India talks about Climate Change, Sustainable Development and Energy

The proposed regulations from the Madhya Pradesh state electricity regulator (draft regulation) has brought the debate of merit-order vs must-run … More

NITI Aayog recently released the draft National Energy Policy (NEP) for public consultation. The NEP has been a work in … More

In the last few weeks two big announcements caught my attention. Incidentally both of them happened to be Electric Vehicle … More

I got an opportunity to speak at the Times Renewable Energy Expo, a Renewable Energy (RE) conference in Pune this … More

A review of the book on electricity reforms by Prayas

Approaching the half-way mark of the 2021-22 targets for Renewable Energy (RE), there was huge expectation from the 2017-18 budget … More

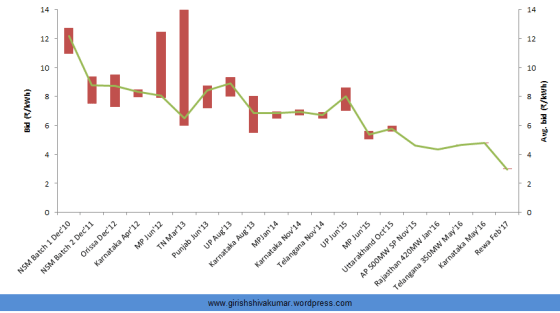

Solar tariffs reaching grid parity was considered the holy grail of Indian Renewable Energy (RE) sector. Starting out in 2010 … More

BP released its annual energy outlook and this year’s projections look into the energy markets up to 2035. As expected, … More

Peenya Industrial Area (PIA) is largest small scale industrial sectors within Bengaluru city. PIA is one of the largest Micro … More