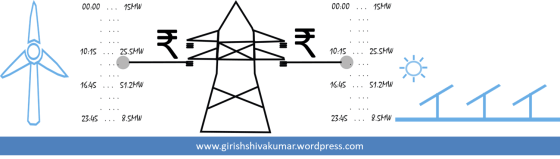

“Wind and solar power projects are powered by natural sources and hence their tariffs should be low”, is a general … More

Girish Shivakumar

“Wind and solar power projects are powered by natural sources and hence their tariffs should be low”, is a general … More

Ministry of Power (MoP) recently invited comments on a consultation paper on issues related to Open Access (OA). Electricity Act … More

The inefficient electricity tariff structure

The reason behind BESCOM’s new tariff proposal