The year 2017 has been yet another landmark year for the Indian energy sector. At a national aggregate level India … More

Girish Shivakumar

The year 2017 has been yet another landmark year for the Indian energy sector. At a national aggregate level India … More

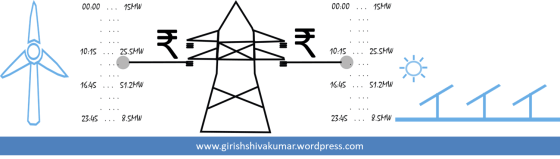

“Wind and solar power projects are powered by natural sources and hence their tariffs should be low”, is a general … More

NITI Aayog recently released the draft National Energy Policy (NEP) for public consultation. The NEP has been a work in … More